|

|

Sysoft ® |

|

|

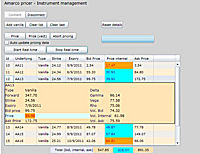

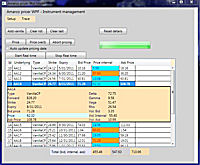

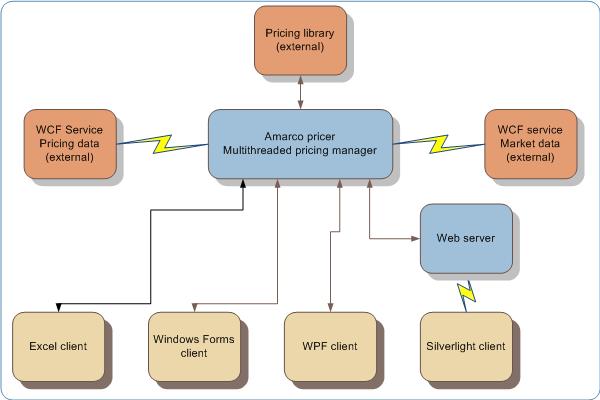

Amarco Pricer Derivatives pricer framework (indices, equities) Using the Amarco architecture concepts and leveraging our trading room activity (design & implement indices and equities derivatives pricers), we designed and developed a working high end multithreaded trader pricing framework, optimized for derivatives pricing instruments (indices and / or equities). It can use as user interface any Microsoft facility: WPF, Silverlight, Windows forms or Excel.

Amarco pricer architecture

This simulates real time data feed through Web services (WCF), replicates the pricing environment feed from back office through another WebService, manages limited computing resources for quants library

Various user interface use the same processing core:

Various animated demos are available, please use the left navigation pane. Microsoft technology used: Multithreaded Excel 2007, Multithreaded Windows forms, Dotnet C# 3.5, Visual Studio 2008-2010, WCF service extensions, WCF services (client, server), VSTO 3.0, Silverlight, WPF.

|

|

HR Web - HR web site with graphics Amarco Pricer How to start using Amarco pricer Amarco grid How to start using Amarco Grid Amarco Informations SysoftSoftware by Cartiant Contact |

|

Copyright (c) Ion Alexandre CARTIANT Sysoft 2004-2023 |